Why Hong Kong Is Winning the Post Hormuz Family Office Realignment

- Apr 26

- 4 min read

Author: Biswajyoti (BJ) Upadhyay

Chairman, Global Transaction Banking Committee

Financial Executive Club (FinEx Club) Research Centre

Research Analyst: Zhao JiaYi Emilia

When the Strait of Hormuz seized up in early 2026, a 97% collapse in tanker traffic, the shockwaves travelled far beyond the Gulf. For the world’s family offices, many of which had long treated Dubai, Abu Dhabi and Doha as their natural homes, the crisis was a reminder that geopolitical geography still matters. Add to that the deepening US–China technological decoupling, and the global map of private capital began to redraw itself almost overnight.

The unexpected winner of this reshuffle has been Hong Kong.

For years written off as a fading outpost — too political for Western capital, too constrained for Chinese capital — the city has re‑emerged as the most dynamic node in the new financial order. Offshore renminbi deposits rose 18 per cent in the first quarter of 2026. Family office registrations jumped 25 per cent in 2025. And the Hong Kong Monetary Authority doubled its RMB liquidity facility to Rmb200bn.

Something deeper is happening than a cyclical rebound. Hong Kong is not merely recovering; it is re‑anchoring itself at the centre of a new capital geography.

A new role: from safe haven to strategic sandbox

For decades, Hong Kong’s pitch was simple: low tax, rule of law, and proximity to China. But in 2026, that formula evolved into something more ambitious.

The city has become a strategic sandbox — a place where capital can experiment with new asset classes, test cross‑border structures, and access Mainland China’s technology economy without being trapped inside it.

The 2026 budget introduced incentives for family offices investing in alternative assets such as art, carbon credits and precious metals. Regulators expanded the Qualified Foreign Limited Partner scheme, allowing foreign capital to trial investments in Mainland tech and green energy under common‑law protections. And the city’s digital‑asset pilots — from tokenised real‑world assets to the m-Bridge cross‑border payments project — have given it a regulatory edge that Singapore and Dubai cannot easily replicate.

Hong Kong, in other words, is no longer a parking lot for wealth. It is a laboratory.

Why Singapore and Dubai fell out of sync

The contrast with Hong Kong’s rivals is stark.

Singapore, long the default choice for Asian wealth, has become a victim of its own success. Regulatory tightening in 2025 raised the bar for family office registration. Asset saturation compressed returns. The city remains efficient, but it no longer feels like a frontier.

Dubai, meanwhile, has leaned heavily on tax incentives and lifestyle branding. Its family office portfolios remain dominated by real estate and infrastructure — stable, but hardly the engines of future growth. For investors seeking exposure to AI, green energy or Mainland China’s industrial upgrading, Dubai is simply too far from the action.

Hong Kong’s advantage is structural: it sits next to the world’s second‑largest economy, yet operates under a legal and financial system that global capital still trusts.

The two‑way valve: Hong Kong’s unique capital architecture

What truly differentiates Hong Kong is its dual‑corridor model — a two‑way valve that channels capital both into China and out to the Global South.

Inbound: Middle Eastern capital into Mainland tech

Gulf sovereign wealth funds, shaken by the Hormuz crisis and eager to diversify away from the US dollar, have turned to Hong Kong as their entry point into China’s technology and green‑energy sectors. Tech listings on HKEX surged 150 per cent in 2025, creating a pipeline of opportunities that Western markets cannot match.

Hong Kong offers what Dubai cannot: RMB liquidity, legal certainty, and direct access to China’s innovation economy.

Outbound: Hong Kong capital into ASEAN, Latin America and Africa

At the same time, Hong Kong is financing the next wave of Global South industrialisation. Supply‑chain corridors linking Shenzhen to Jakarta, Ho Chi Minh City and Mexico City increasingly run through Hong Kong’s banks and family offices. Investors borrow in low‑yield currencies and deploy into high‑growth emerging markets, using Hong Kong as the structuring hub.

This two‑way flow creates a self‑reinforcing loop: inflows generate assets; outflows expand reach; both deepen Hong Kong’s centrality.

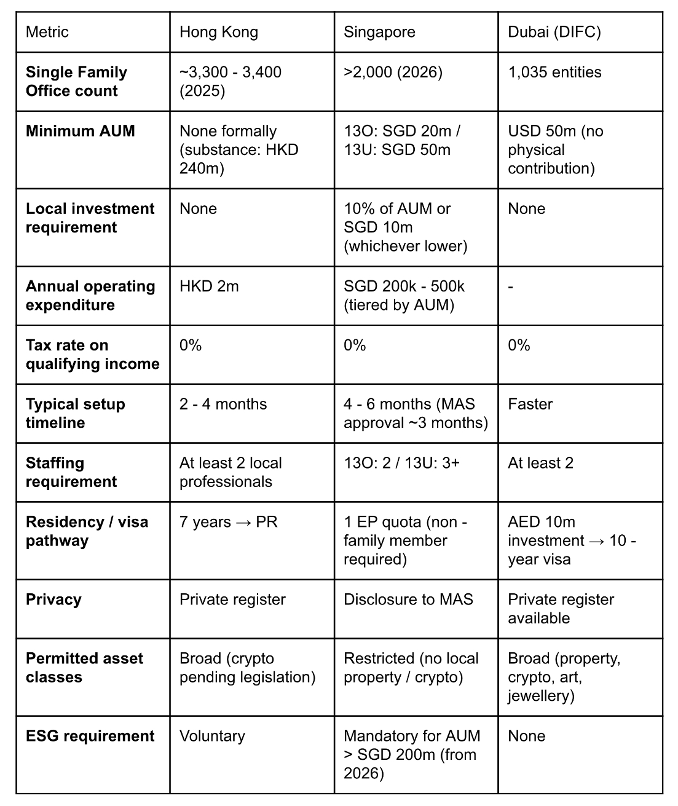

A detailed comparison across these three locations is provided in the Appendix.

The Loop: how Hong Kong anchors mobile capital

Hong Kong’s long‑term strength lies in its ability to convert mobile capital into anchored capital.

The Loop works like this:

1. Capital arrives seeking safety, liquidity and tax efficiency.

2. It is deployed into Mainland tech, green energy and new‑economy listings.

3. Value accretes as these assets appreciate and recycle through HKEX.

4. Profits are reinvested into Global South expansion, creating new deal flow.

This cycle reduces volatility and increases retention — the opposite of Singapore’s one‑way outflow model or Dubai’s one‑way inflow model.

The risks: Hong Kong’s Zheng Yongnian paradox

Yet Hong Kong’s resurgence is not guaranteed.

The city faces what some scholars call the Zheng Yongnian paradox: capital that flows in quickly can exit just as fast. Tax incentives alone cannot anchor wealth. To secure long‑term retention, Hong Kong must embed capital into real‑economy assets — R&D centres, deep‑tech alliances, and tokenised infrastructure.

The next phase of competition will be fought not over tax rates, but over institutional depth: who can offer frictionless cross‑border flows, credible digital‑asset frameworks, and regulatory certainty in a fragmented world.

Hong Kong has momentum. But momentum is not destiny.

A new financial geography

The post‑Hormuz world is not multipolar; it is multi‑corridor. Capital no longer flows along a single axis — West to East, or North to South — but through a lattice of strategic nodes

Hong Kong has positioned itself as one of those nodes. Its dual identity — safe haven and growth platform — is precisely what the new era of private wealth demands.

If it can institutionalise this role, Hong Kong will not merely benefit from the reshuffling of global capital. It will shape it.

Appendix

Recent regulatory and market developments in Dubai, Singapore, and Hong Kong have further differentiated these three financial hubs. Dubai stands out with its zero-tax regime and low entry barriers, Singapore maintains a structured and compliance-driven framework with higher substance requirements, and Hong Kong continues to attract capital through its flexible regulations and direct access to China. The following tables summarise the latest 2026 metrics.

Comments